TD Investment Worthy Startup Weekly

Week 20: 11 May to 17 May 2026

Signal: African startup capital is becoming more architecture-led, with readiness, infrastructure, policy exposure, and liquidity discipline carrying more weight than announcement volume.

Capital Movement: Capital is concentrating around seed-stage bridges, infrastructure-heavy operators, selective secondaries, and targeted facilities.

Infrastructure Trend: Payment rails, EV infrastructure, remittance systems, and merchant tools are increasingly being judged by durability, integration depth, and operating cost.

Regulatory Signal: Kenya’s Finance Bill proposals show that policy risk is now a direct input into startup pricing, margins, and investor diligence.

Signal Recap

This was not a loud week. It was a structural week.

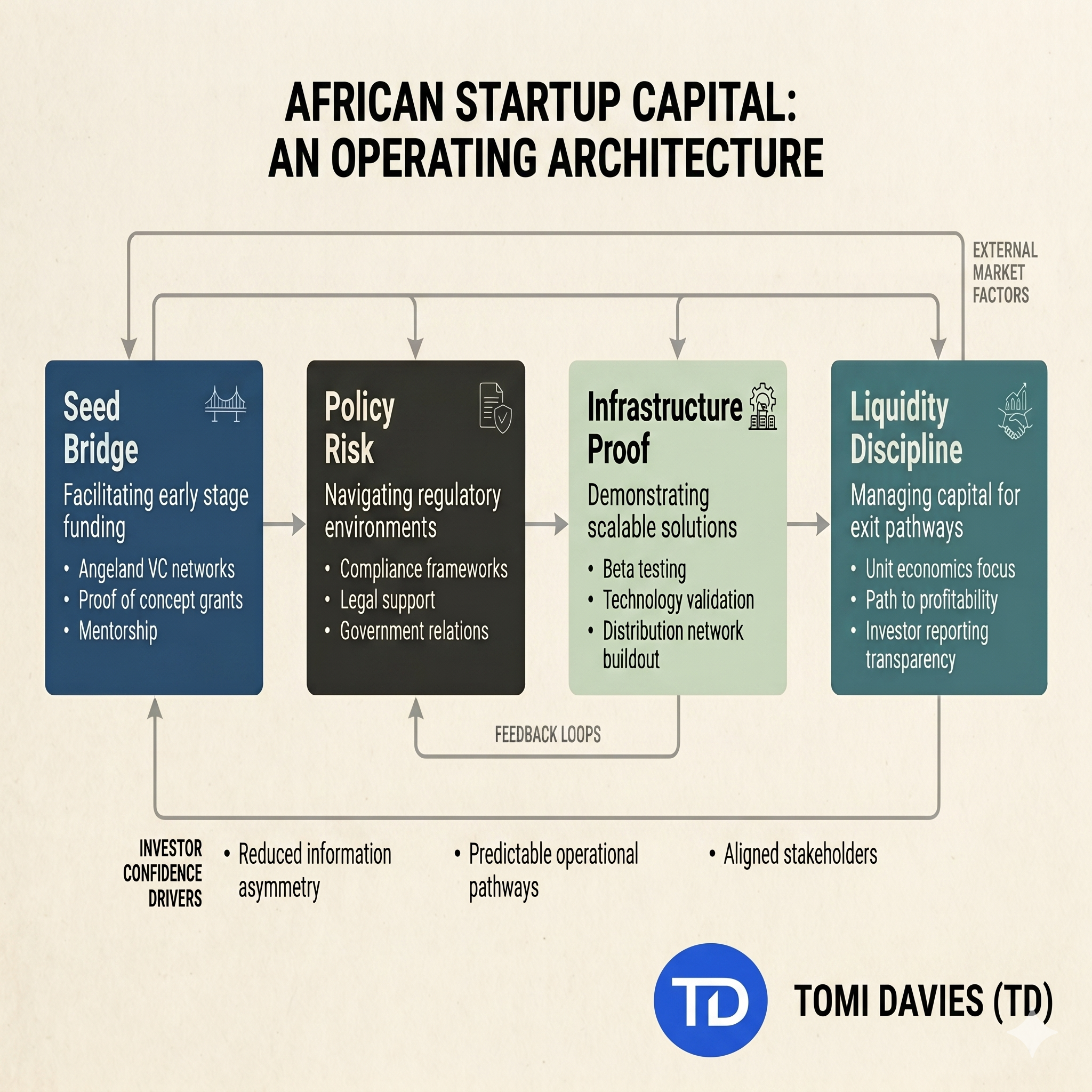

The clearest signal came from the launch of the [Digital Africa DA Seed Fund](https://www.digital-africa.co/en/blog/digital-africa-launches-the-seed-fund). The fund is framed around a familiar gap: startups that have moved beyond pre-seed promise but are not yet credible enough for larger institutional rounds. That gap is often described as a capital gap. I read it as a readiness gap.

Capital is available for some founders, but it is becoming more conditional. It wants traction, systems, governance, execution discipline, and evidence that can survive diligence. That is why the DA Seed Fund matters. Its value is not only the cheque. Its value is the recognition that the seed stage needs structure, not just enthusiasm.

The same week gave us a harder signal through [Chimoney’s shutdown](https://techcabal.com/2026/05/13/chimoney-shutdown-lack-of-capital/). A fintech infrastructure company can be strategically relevant and still fail to raise enough capital to continue. That should sit uncomfortably with founders, angels, and ecosystem builders. If other businesses depend on your rails, your runway is not just your internal issue. It becomes ecosystem risk.

Then Kenya added policy pressure. The proposed Finance Bill measures covering [digital payment rails and software services](https://techcabal.com/2026/05/13/kenya-moves-to-tax-card-networks-and-software-giants/) and [EVs, lithium batteries, and e-bikes](https://techcabal.com/2026/05/14/kenya-vat-electric-buses-two-wheelers-lithium-batteries/) show that regulatory exposure is no longer a footnote. It changes pricing, margins, adoption assumptions, and investor risk models.

There were also constructive signals. [Dodai’s $13 million blended debt and equity round](https://disruptafrica.com/2026/05/11/ethiopian-ev-startup-dodai-raises-13m-series-a-funding-round/) shows that infrastructure-heavy climate mobility can attract capital when the operating model is concrete. [Yoco’s Apple Tap to Pay partnership](https://disruptafrica.com/2026/05/14/yoco-partners-apple-to-bring-tap-to-pay-on-iphone-to-sa/) shows that small-business payment infrastructure is still moving toward lower friction. [Sango Capital’s $120 million secondary transaction](https://www.avca.africa/news-insights/member-news/sango-capital-executes-us-120mn-african-private-markets-secondary-deal/) shows that African private markets need liquidity architecture, not only new fund formation.

The pattern is clear enough: capital is not only asking who is growing. It is asking who is structured.

Implications for Founders

Founders should treat this week as a test of investment readiness.

At ideation stage, the lesson is simple. Do not confuse a large market with an investable proposition. If your model depends on regulation, imported hardware, cloud software, card schemes, public infrastructure, or cross-border flows, your earliest assumptions must include those dependencies. A clean problem statement is not enough.

At pre-seed, the DA Seed Fund signal matters because the bridge between MVP and seed is getting more demanding. Early traction must be organised. Customer evidence should be separated into signed pilots, active users, paid usage, repeat usage, retention, churn, and revenue quality. A founder who cannot separate those categories is asking investors to do their operating work for them.

At seed, Chimoney is the uncomfortable case study. The question is not whether the product was useful. The question is whether the operating system, capital plan, distribution strategy, and runway discipline matched the importance of the infrastructure being built. If your company becomes a dependency for others, you need stronger continuity planning, clearer customer communication, and a more disciplined capital strategy.

At Series A and beyond, Dodai and Yoco point to the direction of proof. Infrastructure-heavy businesses need evidence of utilisation, cost structure, operational reliability, partner quality, and unit-level economics. Partnerships with major platforms help, but they are not proof by themselves. They become proof only when they translate into adoption, retention, and better margins.

Founders should also update their policy-risk files. Kenya’s proposed tax changes are not only a Kenyan issue. They are a reminder that African startups often build on layers they do not control. If your pricing model breaks when tax treatment changes, show that early. If your supply chain depends on imported batteries, devices, or infrastructure, show the sensitivity. If your fintech depends on card networks or foreign software, show the cost exposure.

The founder who can evidence these points will be easier to trust. The founder who hides them behind optimism will slow down diligence.

Implications for Angels and Syndicates

Angels should not read this week as a reason to retreat. They should read it as a reason to become more precise.

The first adjustment is diligence depth. For infrastructure, fintech, mobility, and climate deals, a deck is not enough. Angels need dependency maps. Which providers does the startup rely on? Which licences or exemptions matter? Which tax assumptions affect margins? Which counterparties control distribution? What happens if one rail, partner, or jurisdiction changes terms?

The second adjustment is ticket discipline. If a founder cannot explain the milestone the round funds, the ticket is not yet disciplined. “Growth” is not a milestone. “Expansion” is not a milestone. A milestone is something that can be evidenced inside a data room and assessed before the next cheque.

The third adjustment is reserve logic. In a tighter trust environment, angels should stop allocating as if the first cheque is the main decision. The real question is whether the company can reach a cleaner financing point. If not, the first cheque may only finance a longer uncertainty period.

Syndicate leads need to improve evidence standards before circulating deals. A memo should not simply repeat the founder’s narrative. It should test the claim. It should explain what has been verified, what remains unverified, what the round funds, what the next proof point is, and where the main risk sits.

For diaspora angels, this matters even more. Distance increases information asymmetry. A clean data room, verified traction, governance hygiene, and clear use of funds reduce that distance. Without them, diaspora participation becomes sentiment-led, and sentiment is expensive when it is wrong.

Sango’s secondary transaction also matters for allocators. It reminds us that private capital markets mature when there are ways to rebalance, transfer exposure, and create liquidity. African venture cannot rely only on new-money stories. It needs credible pathways for continuation, exit, and portfolio management.

Second-Order Effects

My inference is that stronger founders will start designing for diligence earlier.

That does not mean they will become more bureaucratic. It means they will become more legible. The advantage will shift toward founders who can show how revenue is earned, how risk is managed, how capital is used, how customers behave, and how the company survives dependency shocks.

A second effect is that ecosystem programmes will face more scrutiny. Accelerators and venture studios can no longer claim success because founders pitched well or appeared at the right events. If founders leave programmes without investor-grade evidence packs, those programmes are creating visibility without readiness.

A third effect is that policy modelling becomes part of founder readiness. Kenya’s proposals show how quickly the operating environment can move. Founders in regulated or tax-sensitive sectors need board-level awareness before they have formal boards. Angels should ask for this early, not after the term sheet.

A fourth effect is quiet but important: liquidity infrastructure may become a more serious conversation. Sango’s transaction suggests that African private markets are developing more tools for managing exposure. That matters because LP confidence is affected not only by entry opportunities, but by the ability to exit, rebalance, or extend intelligently.

The weakest actors will be exposed by this environment. Not immediately, and not always publicly. But slowly. Companies with vague metrics, messy governance, unclear dependencies, weak runway discipline, and poor evidence trails will find the next round harder than the last.

The stronger operators will not need louder stories. They will need cleaner proof.

Concrete Moves

If you are raising in the next 90 days, update your data room before updating your deck. Add current financials, customer evidence, cap table, use of funds, runway, regulatory exposure, tax assumptions, contracts, and the next milestone the round will finance.

If your business depends on payments, software platforms, cloud infrastructure, imported hardware, batteries, or cross-border rails, create a dependency map this week. Show the provider, cost exposure, failure risk, alternative provider, and customer impact.

If you are a fintech or infrastructure founder, prepare a continuity note. State what happens to customers, balances, data, integrations, and service access if you pause operations, fail to raise, or change providers.

If you are building in Kenya or selling into Kenya, model the proposed Finance Bill scenarios. Do not wait for enactment before understanding margin exposure.

If you are in climate mobility, separate adoption demand from asset economics. Investors need to see utilisation, maintenance cost, battery replacement assumptions, import exposure, financing structure, and payback period.

If you are an angel reviewing a deal this month, ask for the milestone the round funds in one sentence. If the answer is vague, pause the allocation conversation.

If you run a syndicate, add a verification section to every deal memo. Use three headings: verified, not yet verified, and material risk.

If you are a diaspora angel, do not invest on founder access alone. Require evidence that travels well: customer proof, governance documents, bank statements or financial reports, contracts, regulatory notes, and clean cap table records.

If you are an accelerator, make investor-grade evidence packs a graduation requirement. Demo day without documentation is theatre with catering.

If you are an ecosystem builder, focus less on producing more pitch events and more on reducing diligence friction. Shared templates, readiness standards, founder evidence clinics, investor memo discipline, and governance education will do more than another panel.

The serious advantage now belongs to the operators who can make trust verifiable.

I trust that helps!